This is your very first post. Click the Edit link to modify or delete it, or start a new post. If you like, use this post to tell readers why you started this blog and what you plan to do with it.

This is the post excerpt.

This is your very first post. Click the Edit link to modify or delete it, or start a new post. If you like, use this post to tell readers why you started this blog and what you plan to do with it.

Are you planning to buy a home or already a homeowner, this online calculator can be of great help in designing your monthly budget and channelize the funds accordingly. Home loan is an affair of lump sum amount of money, a little mismanagement in fund can create a tug of war between your savings and expenditure. Experts advise borrowers to plan their loan term in such a way that they don’t find it difficult in carrying forward the repayment process. Before the introduction of the HDFC EMI Calculator, the borrowers had tough time in calculating their EMIs and tallying them with the payments they make. The mind boggling calculations were often error prone leaving the borrowers at the mercy of the financers in getting the EMI structure, that varied depending on the balance amount, present interest rate (in case of adjustable rate) and remaining installments.

This online calculator increases the transparency in the EMI payments, because when you have an amortized table before you, you can directly approach the financer for your queries with a valid figure. This gives you quantum amount of mental peace; because you know what you are paying and can plan your savings accordingly after keeping the EMIs aside.

The online HDFC EMI Calculator has the following benefits:

The long home loan tenure can be exhaustive or hassle-free; both depend on the amount of preparation you have, to take forward the monthly installments. When you have taken your home loan at an adjustable rate of interest, it is obvious that the rates will fluctuate depending on the market condition, financer & government policies. With the change of interest rate, the EMI also changes, similarly with each installment you pay your balance amount & the number of installments comes down affecting your EMI. All these calculations physically, can lead to bewilderment. So to have an exact idea it is wise to take the help of the budgeting tool available at the finger tips.

You don’t have to go to your financer for getting the tool; it is available at your tips. The financers know that it is a mentally painstaking task, for the internet savvy, sky-rocketing generation, they prefer everything at the finger tips. Keeping this in mind the financers have introduced, this useful budgeting tool; this solves your EMI calculations within a wink. Just visit any aggregator site or the website of the financer and click on the link to HDFC EMI Calculator and feed in the balance amount, interest rate and number of installments and get the EMI easily.

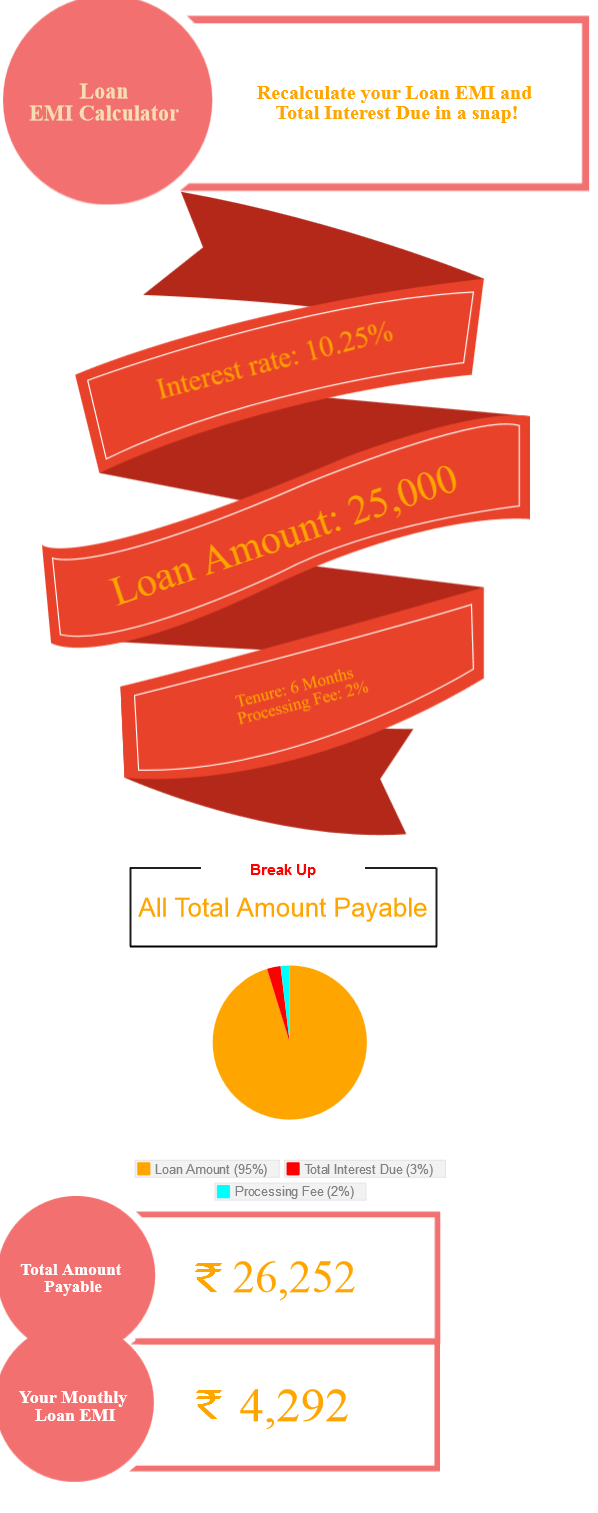

Use the interactive Home Loan EMI Calculator to calculate your home loan EMI. Get all details on interest payable and tenure using the home loan calculator.

Use the interactive Home Loan EMI Calculator to calculate your home loan EMI. Get all details on interest payable and tenure using the home loan calculator.

They say tomorrow belongs to those who plan for it today. It’s a quote that stands true in all walks of life, including your journey as a home loaner. As you may know, taking out a home loan isn’t a decision to be taken blindly; it involves a lot planning and future foresight. And so after you’ve fixed on property you want, the amount you need and probably the financial institute you wish to borrow from, the last and most vital component of planning your repayment remains. Physically jotting down and calculating your repayments is a tedious task to say the least, but there is an easier, more convenient way to do this, the home loan EMI calculator. This article will look at what a home loan EMI calculator is, how it works and what are the benefits of using a home loan EMI Calculator.

So what is a home loan EMI Calculator?

In the not so distant past, one would calculate his or her EMI using a pen and paper or using formulas on Excel. This allowed for a margin of human error and provided an EMI that was, albeit close to the actual EMI, but not 100% accurate to an EMI the bank required you to pay. So as to make this calculation easier for user, most banks and non-banking financial institutes have introduced home loan EMI Calculators in their website. This tool generates an accurate EMI based on your preference in regard to the loan amount you wish to secure, the tenure as to which you wish to take the loan for and the interest you can afford to pay.

How does the home loan EMI calculator work?

Unlike the mentally racking procedure of physically calculating your EMI or using tedious formulas on Excel, leading financial institutes allow you the comfort of arriving at your EMI by just feeding in few details pertaining to your loan on their website. Most home loan EMI Calculator take into consideration the loan amount you wish to secure, the tenure for which you wish to take the loan and the interest you are most comfortable paying to arrive at the EMI you will end up paying. Some institutes might also take into account the processing fee you are comfortable paying. Put in these details into theEMI calculator and an algorithm does the back work to form an EMI amount based on the variables you’ve fed into the calculator. Aside from the installments, leading financial institutes have designed their home loan EMI calculators to provide additional details such as the breakup of the payable amount and the quarter by quarter graph of loan payment estimates.

What are the advantages of using a home loan EMI calculator?

The obvious advantage with an EMI calculator is that you know the accurate amount you’re expected to pay. Braced with this knowledge you can make plans to set aside funds to repay your loan without stressing your wallet. Another salient advantage is the higher approval rate, because of the sound calculations, you can apply for the loan within your financial reach, and seeing this, financial institutes are more comfortable issuing you a loan. The home loan EMI Calculator not only helps calculate EMIs and plan your finances, it also provides you with an element of complete peace of mind.

Now that you’re armed with the precise knowledge procured from the home loan EMI Calculator, all that’s left for you to do is to approach the financial institute of your choice, apply for a loan and enjoy the comfort of your dream house which is now closer to reality than ever.

The amount of money you borrow from the financial institution to invest in some immovable property is termed as home loan. Banks and NBFCs lend money to the borrower at a fixed or an adjustable/floating rate of interest.The home loan is given for the properties like; the already constructed property, flats, under construction property, buildings that are to be constructed over pre-owned properties and renovation of existing property. The amount one can avail depends on the job stability of the borrower, the CIBIL score,the location of the investing property, the listed builders, and the status of the co-borrower. The loan eligibility increases with addition of the earning family member like the spouse, father, mother brother or any earning co-applicant as the guarantor.Due to low rate of interest charged by the banks and NBFCs in comparison to other loans, like the personal loans and education loan, the borrowers make a mistake of applying for a large amount. When the burden of EMI falls then they realize their mistake. To save the borrowers from committing this mistake, lending organizations have come up with the home loan EMI Calculator.

Manually calculating the EMIs with reducing principal amount over the passing yearof the loan term tends to be problematic task. It ends up in a financial mess. Home loan EMI Calculator from different lending organizations is a solution to this problem. The principal amount on which one takes the loan reduces with the payment of EMIs every year. So, the rate of interest also reduces leading to a savings of 0.5-1.0% approximately.

After taking the home loan, the crucial part of the procedure is repayment of the EMIs. So beforehand planning can help the borrower to plan the savings procedure accordingly and complete the process hassle-free. A clear knowledge of the amount to be repaid towards EMI can help to take an informed decision. We should calculate the EMI with the home loan EMI Calculator because, it helps determining the loan amount, it assist in checking the interest percentage, the tenure of the loan can also be determined, it checks the affordability. With the help of the calculator we can compare and select the best lending institution that can offer additional benefit. The decision of taking the fixed or floating rate of interest becomes wiser. Once the EMI amount is decided the selection of the loan will be easier and faster.

It is always commendable to be ready for the wintry days, when the market rate fluctuates, any accidental situation knocks. The accurate calculation which results to a handsome saving can help us to overcome the situation without being enlisted as a defaulter. The home loan EMI Calculator is a boon for the borrowers in the age of recession.

A fair understanding of the ratio of principal amount to the interest due, based on the effect of the home loan tenure and interest rates is provided to the borrower with the use of the calculator.

The calculator will give an approximate figure for the total installment along with complete break-up of the home loan repayment process. The borrower can use it to gain access to an amortization table to strategize the repayment schedule. With EMI calculator a proper calculation of the amount is done before hand, and the repayment can be adjusted accordingly by the borrower.

A very important criterion to be kept in mind while taking a home loan is the Tax Benefit on Home Loan. In the union budget announced on 1st Feb 2017, the Finance Minister has made significant changes with respect to tax benefit on home loan.

So, here we will discuss about these changes and further tax benefits on home loan.

Some points we will discuss here—

Tax benefit on home loan for under construction property before possession

Booking an apartment which is under constructed is sometimes cheaper.

If you have taken a home loan for purchasing under construction property, you can claim tax deduction on the interest paid during the construction year after construction is completed and property possession is given to you but there is no tax deduction on principal repaid during the construction period.

According to Section 24 of IT Act, you can claim deduction against the interest amount that you have paid on your housing property during the pre-construction period.

Tax benefit on home loan for individual applicant

EMI is typically divided into principal and Property Loan Emi Calculator.

Principal is allowed as deduction from your gross total income (subject to an overall cap of 1.5 lakh with other eligible investments).Interest payable on self-occupied property is subject to a maximum deduction of 2 lakh under the head ‘income from house property’.

It can be set off against other income, in the same year. This reduces your tax liability. But to claim this, it is essential that the acquisition or construction is completed within 5 years from the end of the financial year in which the loan was taken; else the deduction will be limited to 30,000.

[Source: testblog.in/regroblog/2017/02/08/tax-benefits-on-home-loan-in-india]

Use the interactive home loan EMI Calculator to calculate your home loan EMI. Get all details on interest payable and tenure using the home loan calculator.

Overview:

One can improve one’s credit score either in a systematic way or by doing simple day-to-day activities. However, for attaining a good score one need follow any hi-tech formula. Simple ways will help you get a good score.

Keep a track of the following points

These simple tips will help you in a great way.

[Source: creditseva.com/blog/work-towards-better-score-simple-yet-effective-ways/]

If you are a financially conscientious individual, you may already know that your credit score is an important three digit numeric expression that is looked upon as a barometer of your financial health. But even those who know all about credit scores and credit reports tend to focus only the three-digit number that is their CIBIL score. It is important to make a constant effort to improve CIBIL score, as it will improve your chances of getting timely credit at competitive rates. But what is most important to have a complete and thorough understanding of the factors that influence your credit score. Here is a summary and respective weightage of the factors that constitute your CIBIL score:

Payment track record- 35%

Any article that you have read about how to increase CIBIL score may have always begun with the need to make timely payments on whatever line of credit you have availed of. This is simply because your payment history is the most important factor that influences your CIBIL score. If you are habitually late in making payments for a considerable stretch at the time of servicing credit, it will have a negative impact on your CIBIL score. Therefore, the first and the foremost rule that you must keep in mind while availing of any type of credit is that it is mandatory to make payments on or before the stipulated date. This is half the job done and will help you increase credit score in the long run.

Credit utilization- 30%

People often wonder why their credit scores don’t improve even though they are making timely repayments. This is probably because of credit utilization- another important but neglected factor that influences the credit score of an individual. Simply put, credit utilization is the amount of credit you are using as against your total available credit. Ideally your credit utilization should not exceed 30%. A lower utilization rate over a time leads to a better credit history and thus an improvement in your CIBIL score. A good way to keep utilization rate low is to keep your credit card debt under check.

Did you know that your oldest credit card can help you keep your credit score high? This is because the age of credit or credit history is a factor that influences your CIBIL score. The longer your credit history the better your chances of enhancing your credit score. So, even if you are not using a credit card that you had taken long back, do not make the mistake of closing it. Make the full payment on it and keep it locked away by all means, but do not relinquish it. This will not only shorten your credit history, it will also enhance your credit utilization.

Amount and timing of new credit- 10%

Each time you make an application for a new line of credit through Emi Calculator, the prospective lender puts in a request with CIBIL to get permission to access your CIBIL report and CIBIL score. A request of this nature is called a hard inquiry. Each time there is a hard inquiry on your CIBIL report, your score comes down by a little. Too many hard inquiries over a short period prove to be detrimental to your credit health. On the one hand, it brings down your credit score and on the other projects you as being “credit-hungry”. A lender is usually wary of lending to those who come across as credit hungry individuals as it increases their risk factor. To avoid coming across as credit hungry, you must try to space out credit adequately. For instance, if you are planning to take a big loan such as a home loan in a year, do not avail of any other new line of credit at least six months prior to it.

Mix of credit-10%

In the modern world credit is available easily. On any given day, you perhaps receive a dozen calls to avail of a personal loan or a credit card. In a moment of weakness, when funds are running low, you may even be tempted to avail of fresh line of unsecured credit. But in the long run, it turns out to be a debt trap that you find difficult to get out of. The first rule of credit is therefore to avail of it only when there is dire need for the same. Unsecured credit such as easy personal loans or an online credit card may seem convenient, but too much of unsecured credit does not augur well for your credit health. To keep your credit score high, you should have a good mix of secured and unsecured credit, as the mix of credit is another factor that influences your CIBIL score. Ideally a home loan with a credit card or two or a car loan with a credit card and a personal loan are considered a good credit mix.

Use the interactive home loan EMI Calculator to calculate your home loan EMI. Get all details on interest payable and tenure using the home loan calculator.